The China-Pakistan Alliance

Introduction

Pakistan and China have had deep political, military economic ties that date back to the formation of the respective countries. Each country benefits from this alliance. From Pakistan’s perspective, China provides Pakistan with military technology and weapons, infrastructure and other financial investment, access to Chinese markets, and support for its geopolitical objectives. For China, Pakistan provides China with an all-weather ally, with one way to thwart India’s rise, access to the Indian Ocean through the China-Pakistan Economic Corridor, access to Gwadar Port, which may partly serve as a future Chinese naval base, a place to showcase its Belt and Road Initiative, access to Pakistani markets, and shared intelligence. Given the wide range of benefits that each country derives from their alliance, it is expected that the relationship will continue to be robust.

The Creation of the India and Pakistan

When the British Raj ended, independence was granted to India and Pakistan as two separate states divided along religious lines. The partition resulted in one of the largest mass migrations of history with approximately 10-14 million people crossing the newly formed borders to reach the country of their religious affiliation. A 1951 Pakistani census counted 7,226,600 displaced citizens, the majority of whom were Muslims who crossed the line from India to Pakistan. Similarly, the 1951 Indian census counted 7,295,870 displaced people, the majority of whom were the Hindu and Sikh population that crossed the border from Pakistan to India after partition. Large scale violence accompanied the refugee crisis, with deaths estimated at between several hundred thousand and 2 million people. Most of the violence occurred in the previously British province of Punjab. Punjab, post-partition, was split into West and East Punjab, with the Hindu and Sikh populations migrating to the eastern bloc and the Muslim population moving to the western bloc. There were very few Muslim survivors in East Punjab, or Sikh or Hindu survivors in the Western Punjab region.

Geography of Pakistan

Map of Pakistan

The Islamic Republic of Pakistan is the world’s 33rd largest country by area at 881,913 square kilometers. Pakistan is bounded by India in the east, by Iran in the west, by Afghanistan in the northwest, and by China in the northeast. In the northwest, the Afghan’s Wakhan Corridor – measuring between just 13-30 km in width – separates Pakistan and Tajikistan. In the south, Pakistan has a 1,046 km coastline along the Arabian Sea and the Gulf of Oman and shares a maritime border with Oman.

Its borders with India and Afghanistan are unsettled. Pakistan has fought multiple wars with India and numerous skirmishes with Afghanistan to resolve these border disagreements. However, these borders are still contested despite the previous conflicts. Pakistan’s land incorporates both the Khyber and Bolan Passes, through which wind traditional migration and trade routes that have historically linked Central Eurasia and South Asia. Pakistan has four provinces – Baluchistan, Khyber Pakhtunkhwa, Punjab, and Sindh, two autonomous territories – Azad Jammu and Kashmir and Gilgit-Baltistan, and one federal territory – Islamabad Capital Territory. Additionally, Pakistan asserts that the union territories of Jammu and Kashmir and Ladakh – controlled by India since 1947 – should be under its sovereignty.

Provinces and Territories of Pakistan

In 2019, Pakistan was the world’s fifth-most populous country, with an estimated 205 million people. This represents over a six-fold increase since partition, when its population was just 33 million. By 2030, Pakistan is targeted to overtake Indonesia as the world’s largest Muslim majority country. In 2010, slightly over half its population was below the age of 30 years. Its fertility rate is currently 2.68.

Overall, Pakistan is considered a subtropical country. About 88% of its land is semiarid to arid, receiving no more than 250 mm annual rainfall. Deserts represent approximately 14% of the total of the arid landscape. Its four most significant deserts include the Thar, the Cholistan, the Thall, and the Kharan.

Deserts of Pakistan

Pakistan is divided into three major geographic areas: the Northern Highlands, the Baluchistan Plateau and the Indus River Plain, with the plain’s two major subdivisions corresponding roughly to the provinces of Punjab and Sindh. The Northern Highlands include parts of the Hindu Kush, the Karakoram, and the Himalayas, and is home to five of the world’s fourteen tallest mountains, including K2, the world’s second highest.

Pakistan’s Baluchistan Plateau has altitudes ranging from 600-3010 meters and covers 347,190 km2. The plateau is subject to frequent seismic activity as the plateau sits atop where the Indian plate collides with the plate under Eurasia. The Indian plate is continuing to move northward, thrusting the Himalayas higher by an estimated 40 cm per century.

Pakistan’s third geographical area is the Indus River plain. The Indus River flows through the heart Indus River plain which was created by river silt deposits laid down over the centuries. All of Pakistan’s major rivers—the Kabul, Jhelum, and Chenab—flow into the Indus River as it travels southward. The plain has a catchment area of almost 1 million square kilometers. This plain has been inhabited by agricultural civilizations for at least 5,000 years, including the Indus Valley civilization or Harappan civilization which dates to as early as 2500 BCE. Today, the Indus River Plain also forms the core of Pakistan’s agricultural land. Overall, less than 20% of Pakistan’s land is suitable for intensive agriculture. Its remaining land is defined geographically by mountains, high plateau, and deserts, all of which yield little food.

Geography of Pakistan

From a geopolitical point of view, Pakistan’s geography presents many challenges. Most of Pakistan’s political borders fail to align with any natural geographical boundaries which would make them easier to defend. Similarly, Pakistan’s borders do not follow any clear ethnic divisions. Instead, its boundaries were drawn to separate as nearly as possible the majority Muslim and the majority Hindu populations of the Indian subcontinent.

Pakistan’s greatest geopolitical rival is India, and it is with India that its borders have the fewest geographical defenses. In disputed Kashmir, India currently holds the geographical advantage, including in the Siachen Glacier which is also contested with China. If Pakistan could gain control over all of Kashmir, it could put in place a more formidable mountain defense line in its northeast. Instead, the mountain defense that Pakistan does control in Pakistan occupied Kashmir is in its northwest, located far from Pakistan’s major population centers. Furthermore, many of Pakistan’s most significant cities (and population centers) are located along the Indus River Valley, leaving them exposed if India were to attack. Pulling populations to the west of the Indus River for defense in time of war would mean that Pakistan would be ceding half its country and much of its arable land to India.

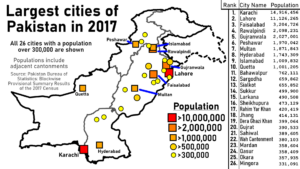

Pakistan’s largest cities

Along its coastline, Pakistan is also vulnerable. It has only a few significant ports, that if blockaded, would effectively transform Pakistan into a landlocked country. Karachi, alone, handles approximately 60% of Pakistan’s cargo, making it a very strategic target.

On its border with Afghanistan, the British drawn Durand border line between Afghanistan and Pakistan is also in dispute. In particular, the line divides historical Pashtun tribal areas. Afghanistan has long dreamed of uniting its 43 million Pashtuns with Pakistan’s 15 million Pashtuns. To this effect, Afghanistan lays claim to a border that extends significantly east of the Durand Line. As recently as 2017, the president of Afghanistan has said that Afghanistan will never accept a border between the two countries that splits the Pashtun tribal area in two. Indeed, when Pakistan applied to join the United Nations in 1947, because of the tribal land dispute, Afghanistan was the only country to vote against Pakistan’s membership application.

Kyber Pass – One of several Afghan-Pakistani mountain passes

Therefore, Pakistan faces countries on both sides of its borders that openly claim land to which Pakistan has effective or aspirational sovereignty. This makes Pakistan vulnerable to a two-front war if India and Afghanistan ever formed an alliance. Complicating the border dispute is the fact that part of the border with Afghanistan runs through the very mountainous Pashtun tribal lands. The rugged mountainous geography makes the border very difficult to police for both countries. Drug smugglers, terrorists, traders, and refugees regularly cross the border undetected in both directions. This makes the Pakistani-Afghan border one of the most unstable and violence-prone borders in the region.

Pakistan’s border with Iran cuts through the arid and sparsely populated region of Baluchistan, also dividing the Baluchistan people between the two borders. In general, Iran and Pakistan cooperate to eliminate Baluchistan separatist movements in their respective areas. However, relations between Iran and Pakistan are complicated by the fact that Iran is predominantly Shia Muslim while Pakistan is predominantly Sunni Muslim. (Pisenti, 2020)

The Kashmir Conflict

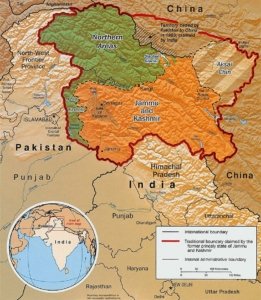

Besides creating various border disputes, the India-Pakistani partition also created a conflict regarding the ownership and sovereignty of Kashmir that remains unresolved to this day. Kashmir is a 138 km² ethnically diverse region located in the western section of the Himalayan range. It is renowned for its scenic lakes, meadows, and snowcapped mountains. At the time the partition, both India and Pakistan each argued that they had sovereignty over the entire princely state of Jammu and Kashmir. Instead, the region was partitioned with India controlling approximately 55% of the area including the Kashmir Valley, most of Ladakh, the Siachen Glacier and 70% of its population. Pakistan has sovereignty over approximately 30% of the land that includes Azad Kashmir and Gilgiyt-Baltistan. In 1963, Pakistan ceded to China about 15% of its recognized territory including Askai Chin (claimed by India) as well as the mostly uninhabited Trans-Karakoram Tract (claimed by India) and part of Demchok sector. The disputed line dividing the Indian and Pakistani regions is called the Line of Control while the line dividing the contested region between India and China is called the Line of Actual Control.

Srinagar, the largest city of Kashmir

Division of Kashmir into Areas of Control: Pakistan-Green; India-Orange; China-Gold

Overall, Kashmir is approximately 67% Muslim, 30% Hindu, 2% Sikh and 1% Buddhist. Kashmir Valley – constrolled by India – is home to approximately 30% of Kashmir’s population; this population is 95% Muslim while Ladakh, home to 6% of the region’s population, is 47% Muslim. (Jammu and Kashmir Official Portal, 2001). Most Muslim would prefer to reside within Pakistan as opposed to India. There has been unrest and violence in the Indian-administered side of Jammu and Kashmir for 30 years due to Muslims desire for political change and India’s repression of their efforts. That said, both countries have committed atrocities and human rights abuses against people living within their areas of control.

Since partition, three wars have been fought over the territory: the Indo-Pakistani wars of 1947-1948, 1965 and 1971. Additionally, in 1989, 2010, 2016 and 2019 the region has been rocked by protest movements. Largely these have been driven by Muslim Kashmiri separatists calling for the right to self-determination.

Indus River and its Tributaries

In addition to ethnic discord, water insecurity is also driving the Kashmiri conflict. The Indus River is the only River system providing water to Pakistan; otherwise 92% of Pakistani land is arid or semi-arid. In India, the Indus is one of two river systems supporting India’s Northwest including the regions of Punjab, Haryana, and Rajasthan, all of which have inadequate water supplies. Punjab produces more than 20% of India’s wheat, and is considered one of India’s bread baskets.

Indus River – Kharmang District, Pakistan

The Indus originates on the Tibetan plateau and then courses 3,200 km southward through India, into Pakistan where it travels the entire length of the country before emptying into the Arabian Sea. India and Pakistan have both extensively dammed the Indus to generate hydroelectricity and irrigation.

The Indus has five important tributaries: the Jhelum, the Chenab, the Ravi, the Sutlej, and the Beas all of which either originate in Indian controlled territory or flow through India’s state of Himachal. Based on the current de facto Line of Control, India is currently the upper riparian country of the Indus and all its tributaries. This makes Pakistan vulnerable if India decides to increase its usage of or restrict the water supplies of the river system. In 1948, for a short period, India purportedly cut off Pakistani water supplies although India vociferously denies this.

Map of the Indus River Tributaries

In 1960, The Indus Water Treaty was agreed between the two countries, allowing Pakistan to have exclusive rights over the three western tributaries of the Indus – Jhelum, Chenab and Indus while India was given control over the three eastern tributaries Sutlej, Ravi, and Beas. For several decades thereafter, the water sharing agreements seemed to satisfactorily meet the water needs of each country. However, the subsequent significant increase in both the Pakistani and the Indian populations has meant that these shared water resources are seeing growing stress. Tensions caused by these diminishing per capita water resources are further aggravated by the distrust between the two countries, by the fact that India is not always forthcoming with its upstream water data, and by India’s construction of a cascade of dams on the Jhelum and Chenab rivers. The Indus Water Treaty allows India to build run-of-the-river dams to generate hydropower on these Pakistani-controlled tributaries if India does not impound water or impede its downward flow. While it would be extremely difficult for India to violate the terms of the Indus Water Treaty, having Pakistan’s water lifeline under India’s control is a strategic vulnerability that Pakistan would prefer not to tolerate.

China’s Part in the Kashmir Conflict

Insofar as Pakistan has been an enemy of India, it has been an ally of China. After the People’s Republic of China was formed, Pakistan was the first Muslim country to recognize its status. China’s early diplomatic shift to Pakistan was driven to some extent by the 1959 Tibetan uprising, and the Dalai Lama’s asylum in India. India’s decision to grant refuge to the Dalai Lama has greatly affected the Sino-India relationship as did China’s perception that India supported the Lhasa uprising. Pakistan was quick to take advantage of the schism, including by leveraging its relationship with China to further its objectives in Kashmir.

Nanga Parbat Peak In Kashmir, Ninth Highest Mountain on Earth

For its part, China has not advocated a concrete policy on Kashmir. Instead, it shifts its position to benefit its own objectives. That said, China’s policy has historically been tilted toward Pakistan. China and Pakistan’s 1963 treaty, for instance, put China on record disputing that India had sovereignty over the entire disputed Jammu and Kashmir region. Pakistan rewarded China for this position by ceding to China land that China considers strategically important. China has since helped Pakistan translate Pakistani claims of sovereignty over its occupied portions of Kashmir into facts on the ground through China’s participation in the construction of the Sino-Pakistani Karakoram Highway that weaves through Pakistan occupied Kashmir.

Karakoram Highway, Passu, Pakistan

The highway has both strategic and military importance to both China and Pakistan. Now, as part of the China Pakistan Economic Corridor Agreement, the two countries are rebuilding and upgrading the highway so that it can provide for three times the traffic, can accommodate heavily-laden vehicles, and it can better operate under extreme weather conditions. China and Pakistan are also planning to link the upgraded highway to the southern port of Gwadar. China views Gwadar as having key commercial and military strategic advantages, particularly as China expands its naval presence into the Indian Ocean.

In addition to the construction of the highway, China has also indicated interest in constructing railway lines, oil and gas pipelines and additional road networks throughout Pakistan occupied Kashmir. To defend these investments, China has been gradually expanding its military presence in Pakistan both by having some troops on the ground, and by satellite and other technological monitoring. This expanded Chinese military presence in Pakistan also better positions China to respond to any Pakistani-based Uyghur agitations that might attempt to disturb China’s current clampdown on its Uighur population in Xinjiang. China’s involvement in Kashmir has also served as a means for China to frustrate India’s ambitions.

In 2019, India increased the stakes in Kashmir by abolishing Article 370 of the Indian Constitution which had provided Kashmir with semi-autonomy. While the autonomy protected by Article 370 in many ways has been more illusory than actual, it has been important point of fact for Kashmiri Muslims. Article 370 afforded Kashmiris their own constitution, a separate flag, and freedom to make laws including those regarding permanent residency and ownership of property. By abolishing Article 370, Kashmiris can no longer prohibit Indians from outside the state to settle there or purchase property. As China has done in Tibet and in Xinjiang, many Kashmiris fear that the Indian government will use the new property laws to change the demographic character of the Muslim-majority region.

The constitutional bill abolishing Article 370 also divided the Indian controlled territory into two, smaller, federally administered territories. One state will combine Muslim-majority Kashmir and Hindu- majority Jammu; the other states creates a Buddhist-majority Ladakh, which shares cultural ties to Tibet. India hopes that creating these two new states will help it further tighten its hold on the territory. However, it will also likely diminish the effectiveness of the two states as buffer zone between Pakistan and India.

India’s abolition of Article 370 is likely to also engage China further in the issue. From the outset, China has supported Pakistan’s protestations of India’s unilateral move for diplomatic reasons. Not only is Pakistan one of China’s closest allies but supporting the Muslim state of Pakistan’s stance on Kashmir helps to divert attention away from China’s crackdown on Muslims in its own territory. Additionally, China has strategic issues at stake. India’s new state of Ladakh’s includes land that Pakistan turned over to China in their 1963 agreement.

China, Pakistan, and Geopolitics

A common refrain shared between China and Pakistan to describe their alliance is “Pakistan-China friendship is higher than the Himalayas, deeper than the ocean, sweeter than honey, and stronger than steel.” For Pakistan, China has proven a highly beneficial partner. Like Pakistan, China also considers India a strategic rival and is motivated by actions that contain India’s rise. China is Pakistan’s largest source of foreign direct investment. Chinese investment in Pakistan totals more than any other Belt and Road country, exceeding an estimated $32 billion from 2014-2018. In 2020, China committed an additional $11 billion to the construction of two hydropower generator projects in Kashmir and another $7.2 billion to upgrade Pakistan’s railways in their entirety. China also provides Pakistan with a steady stream of military technologies and equipment. Pakistan and China intend to use this military technology to partly fill the security vacuum being created as the West completes its withdrawal from Afghanistan.

Karakoram Highway connecting China and Pakistan

Additionally, the Pakistani military benefits from the steady stream of military material. Pakistan’s military has played an important role within the Pakistani political system since Pakistan’s inception in 1947. Since its founding, Pakistan has experienced three military coups, and has been under military rule for more than half the time. Even when a democratically elected government is in place, the military remains firmly behind the scenes. Pakistani military leaders believe the civil government provides the military with political legitimacy, while still allowing the military to play an important role in the Pakistani polity and economy. Elected leaders and the civil government balances the power of the Pakistani military. That said, politicians also nurture their own military relationships to facilitate their efforts to remain in power.

The JF-17 Thunder is a joint Pakistan-China project.

The Pakistan military benefits significantly from its position within Pakistan. The military receives an abundant budget that does not receive any oversight. Among other line items, this budget provides the Pakistani military with its own system of schools, healthcare, housing, and pensions. It also provides the military with the funds to invest in economic activities. In 2005, for instance, it was estimated that the military held over $130 billion of assets in listed companies.

The Pakistan military has profited from strong ties with China. Firstly, China sells Pakistan a wide arrange of military technology and equipment, often at deep discounts. Pakistani officers have been known to benefit personally from these defense deals by taking a cut for themselves. Secondly, Pakistan’s generals know that authoritarian China will not criticize the military when it acts upon democratic institutions. On the contrary, China has been providing the Pakistani military with technology including facial recognition, monitoring, smart alert systems and other surveillance technology. For instance, China has offered Pakistan the option to use Beidou – China’s GPS equivalent. Beidou would provide Pakistan with the ability to track its citizens with the same rigorousness employed by China. As a result, Pakistan has been trending toward greater political repression with Chinese technology and media content expediting this trend.

A new, Chinese-built, fiber-optic network now links the two countries, including a connection to newly installed undersea cables at Gwadar. Among other benefits, this network will facilitate Pakistani control over television and programming content and its distribution, improving its ability to frame political narratives. As a side benefit to China, the network enables China to distribute pro-China programming more effectively.

Gwadar Port

The Pakistani military also benefits from its relationship with China through its military construction unit, the Frontier Works Organization (FWO). Specifically, FWO gets first look at all China-Pakistan projects. FWO’s ties to China are strong and long-standing. In 1966, for instance, FWO worked with China to build the original Karakoram Highway. Currently, the FWO is benefiting from China-Pakistan construction contracts in the infrastructure, power, oil, real estate, mining, and railway sectors. For instance, the FWO has been constructing roads that link the Gwadar Port to the rest of Pakistan’s highway network. These construction contracts may provide further opportunities for military self-enrichment.

For China, Pakistan is one of its most trusted geostrategic alliances. Functionally, Pakistan provides China with many benefits. Firstly, Pakistan provides China with one way to bog India down at its borders. Regional land skirmishes mean India must divert resources away from power projection into the Indian Ocean just as China is trying to sail into it. The skirmishes keep India off balance, sidetracked, depleting energy that could otherwise be focused on China or abroad. The Sino-Pakistani alliance also helps China balance against the tightening US-India relationship. The China Pakistan Economic Corridor also acts as a political tool to frustrate any attempts either India or Pakistan might make to improve their relationship by making Pakistan reliant on China for technology and financing.

Pakistan benefits China secondly by providing it with an important Belt and Road network branch, enabling China and its western region to gain additional access to global centers of energy production, natural resources, and economic markets. This branch links China’s western interior regions to Gwadar Port and the Indian Ocean. Overland westward expansion provides China with an ability to escape the confines of East Asia while minimizing outright confrontation with the United States and its Asian allies.

Current linkages between Pakistan and China include roads, dams, and fiber optics. Future Sino-Pakistani linkages projected include rail, other technology networks, and energy pipelines. These pipelines will create a second route for Middle Eastern and African oil and gas to travel to China.

The Pakistani Belt and Road branch also helps to showcase the benefits of China’s Belt and Road Initiative to the global community.

Thirdly, Pakistan provides China with two naval bases in the Indian Ocean, the Karachi and the Gwadar Ports. China is seeking to project naval power into the Indian Ocean, through the Persian Gulf, into Mediterranean Sea, out into the Atlantic, and back to home bases in the Pacific. To do this, China needs a network of ports.

Finally, Pakistan’s intelligence services provide China with intelligence on global jihadist networks. This is an asset as China navigates its own Muslim separatist movements and its deepening involvement in the Islamic world.

China’s strategic sea lanes

Despite the benefits, the Sino-Pakistani alliance has its problems, and each country has its concerns about the other. For instance, while it is a purported Pakistani military strategy to back terrorist attacks against India, China worries about the risks that come when the state-sponsored terrorism blurs lines of responsibility. In the case of the Mumbai attack, for instance, where Pakistani terrorists instigated the attack and displayed military training, China shied away from publicly taking Pakistan’s side. From Pakistan’s perspective, there is concern about exactly how much involvement that Pakistan wants China to have in its economy, military, and politics.

China, Pakistan, and the Nuclear Bomb

After India tested its first nuclear bomb in May 1974, Pakistan accelerated its own nuclear program. By the early 1980s, Pakistan was running a secret uranium enrichment facility, and is believed to have developed the ability to build a first-generation nuclear device. Shortly after India conducted its second nuclear test in 1998, on May 28, 1998 Pakistan discharged five nuclear devices causing it to become the ninth country to possess nuclear weapons in addition to the United States, Russia, France, the UK, Israel, India, China and North Korea. It is believed that Pakistan now possesses between 150 and 160 nuclear weapons, and that its arsenal is still growing. Pakistan is not a signatory to either the Treaty on the Nonproliferation of Nuclear Weapons and the Comprehensive Nuclear Test Ban Treaty. It is currently the sole country impeding negotiations of the Fissile Material Cut-Off Treaty.

Nuclear Fusion

In its journey to acquire nuclear weapons, Pakistan obtained aid from several other states, including China. As early as the late 1970s, China provided Pakistan various levels of nuclear and missile-related technologies. After 1980, Pakistan’s illicit nuclear sourcing network expanded to include Iran, North Korea, and Libya. As Pakistan acquired additional nuclear technology, it shared that technology with China for reverse engineering. In this way, the Sino-Pakistani nuclear collaboration provided technological benefits for both countries.

By assisting Pakistan to develop the bomb, China effectively provided for Pakistan’s security without ever needing to promise to intervene militarily on Pakistan’s behalf. Instead, China gave Pakistan the ultimate way for Pakistan to defend itself. If military ties are at the core of the Sino-Pakistani relationship, China’s support for Pakistan’s nuclear program has been at the core of the Sino-Pakistani military alliance. The nuclear program has created a real level of trust between the Pakistani and Chinese militaries that may not have been achieved if the two countries had a more conventional security partnership. From China’s point of view, both Pakistan and China share a common strategic concern about India’s economic and military rise.

By keeping Pakistan militarily strong, China is also benefiting by making it more difficult for India to project military power abroad, instead keeping it bogged down closer to home. China also benefits economically by being one of Pakistan’s most important arms suppliers. For instance, in addition to nuclear technology, China has also sold Pakistan a wide array of missile technology. Recently, China has been supplying Pakistan with smaller, tactical missile prototypes designed to attack Indian targets in a more limited way, making the idea of a targeted use of a nuclear weapon more credible. These short-range weapons were specifically designed to make it difficult for India to inflict rapid, punitive strikes against Pakistan in retaliation for incidents such as the Mumbai bombing, which was carried out by Pakistani-based terrorists.

Pakistan has not made explicit its formal nuclear doctrine. This means there is ambiguity regarding the circumstances which Pakistan would deem it necessary to deploy its nuclear weapons. Pakistan has stated, however, that its nuclear weapons are meant solely as an anti-Indian deterrent and would be employed only if Pakistan faced an existential threat from India. Pakistan has subsequently clarified that it considered existential threats to include India’s conquest of Pakistan’s territory or military, efforts by India to strangle Pakistan’s economy or attempts by India to destabilize Pakistan domestically.

Pakistan’s missiles on display in Karachi

Of key concern to the international community is Pakistan’s ability to keep its nuclear weapons secure from terrorist groups or other militants. Pakistan maintains that it has complete control over its nuclear weapons, and that it has taken steps to prevent radicalized individuals from infiltrating its nuclear program.

Pakistan has remained critical of the US-India nuclear cooperation agreement signed in 2008. This deal has also caused China to be wary of India’s closer relations with the United States. In response, China has increased its civilian nuclear cooperation with Pakistan. Specifically, China has agreed to supply Pakistan with two, 340-megawatt power reactors. These reactors are additional to the two nuclear power reactors that China has already helped Pakistan build. China has justified this additional nuclear cooperation stating that additional reactors were grandfathered in its 2003 Sino-Pakistan treaty. This treaty was in place before China joined the Nuclear Suppliers Group in 2004.

Sino-Pakistan Economic Relations and the China Pakistan Economic Corridor (CPEC)

The foundation of the Sino-Pakistani relations has always been more about geostrategy than it has been about economic exchange. Close political and security ties were never going to be an assurance of close economic ones, but there has been an expectation that the political and security alliance could be transitioned into a mutually beneficial economic alliance. Everything from geography to cultural preferences have been cited to explain the weak economic relationship between China and Pakistan. One issue has certainly been that the economies lack complementarity. For instance, China competes with Pakistan in textiles, which is Pakistan’s largest manufacturing sector, accounting for 8.5% of Pakistan’s GDP, employing approximately 45% of the total labor force, and 38% of its manufacturing workers.

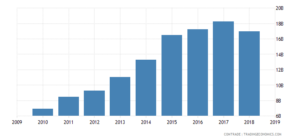

That said, China is an important trading partner for Pakistan. According to the State Bank of Pakistan, Pakistan’s exports to China were $1.9 billion in 2019, representing 8% of total Pakistani total exports. Major export items include cotton yarn, rice, other agricultural products, alcohol and other spirits, copper and related products and chromium ores.

Pakistan’s exports to China

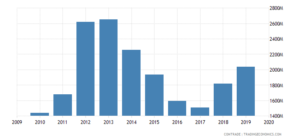

To strengthen their alliance by strengthening their economic relationship, China and Pakistan signed a Free Trade Agreement (FTA) in November 2006, which came in effect in July 2007. Since the FTA agreement went into effect, Pakistani producers have found that, in many instances, the FTA has brought greater advantage to China than it has been to Pakistan. The experience of Pakistani producers has been supported by trade data: since the free trade agreement went into effect, Pakistan’s trade deficit with China has increased from approximately $2.9 billion in 2008 to $12 billion in 2016. Additionally, the FTA has had a negative impact on many of Pakistan’s small and medium enterprises.

China exports to Pakistan

Following on from the FTA, in 2015 China and Pakistan announced the China-Pakistan Economic Corridor (CPEC) project, which China considers to be an essential part of its One Belt One Road Initiative. As of 2017, CPEC projects – both current and future – have been valued at $62 billion. That said, there is a significant gap between the total level of financial assistance pledged and the amount China has actually been provided. (Small, The China-Pakistan Axis: Asia’s New Geopolitics, 2015)

The CPEC will connect China’s Kashgar and its western interior regions to Pakistan’s Gwadar Port, which is being operated by the China Overseas Port Holding Company, a state-owned Chinese company. The CPEC connections include a series of infrastructure and other projects. These projects comprise everything from upgrading Pakistan’s road and rail transportation systems, to enlarging its hydro-engineering networks, to laying fiber-optic cable systems, to increasing Pakistan’s access to technology, to expanding its energy networks. The CPEC also envisages creating a network of Pakistani industries and industrial parks, as well as potentially creating programs that help diminish poverty, encourage tourism, and enhance education, public health, and Chinese-Pakistani people to people communication.

Chinese-Pakistani trade along the Karakoram Highway

Currently, 60% of China’s oil is shipped from the Persian Gulf through the Malacca Straits to Shanghai, a voyage of more than 16,000 km. One benefit China is hoping to derive from the CPEC is to create alternative distribution networks for bringing oil and natural gas into the country. While Pakistan has little in the way of resources, and has no gas or oil, it does provide China with an excellent geographical position in which to access oil from other parts of the world.

In terms of technology sharing, it is expected that a full system of monitoring and surveillance like those in China in cities will also be installed in important CPEC Pakistani cities from Peshawar to Karachi. The envisioned Pakistani fiber optic network will not only improve Pakistani internet access but will also be effective in disseminating television content that is favorable to China. Disseminating China-friendly content is consistent with China’s larger objective of promoting its image and its messaging internationally through global media. To this effect, Beijing is making investments into all sectors of global media, stated that it plans to grow overseas media staff tenfold by 2016, and plans to invest an additional $6.6 billion globally into the sector.

In addition to expanding its media presence globally, China has also been constructing Confucius Institutes internationally. Confucius Institutes seek to teach Chinese, enable cultural exchange, and improve China’s relations with other countries. With regards to China-Pakistan relations, there has been a significant expansion of Mandarin language schools in Pakistan; Pakistan is seeing Mandarin begin to rival English as the most common foreign language taught in the country. These language academies are financed by both the Chinese and Pakistani governments.

Chinese and Pakistani border guards

The CPEC also envisions China engaging in all aspects of Pakistan’s agricultural sector to promote the Pakistan’s transition from traditional to modern, large-scale agriculture. Chinese companies are expected to provide seeds and fertilizer, to run farms on leased or purchased land, to improve irrigation networks, and to establish transportation and storage systems for agricultural produce. In 2017, agriculture accounted for approximately 26% of Pakistan’s GDP and employed approximately 40% of its labor force. This agriculture is supported by one of the world’s largest irrigation systems. Many Pakistani farms are small, although Pakistan also has bigger farms owned worked by tenant farmers who could be at risk of displacement if Pakistan’s agriculture become more commercialized. Given the importantance of agricultural to Pakistan’s economy and employment base, China’s proposed involvement in the sector has been controversial.

While the CPEC will undoubtedly bring significant benefits to Pakistan including upgrading its transportation system, expanding its electrical grid, and improving its hydro-engineering systems, it is likely that China will benefit most from the agreement. Chinese companies such as Haier, China Mobile, Huawei and China Metallurgical Group Corporation view the CPEC as an opportunity to expand their presence in the Pakistani market, while new Chinese companies plan to leverage the corridor to get a foothold into the Pakistani market.

Huawei, for instance, is becoming Pakistan’s most important telecoms infrastructure operator and ZTE, Huawei’s state-owned counterpart, is one of Pakistan’s largest telecoms vendors. It is part of China’s strategy to install information and telecommunication networks along with their corresponding hardware, software and standards throughout Belt and Road Initiative countries to wield more political clout. Already, in many places in the world, China is becoming a leading provider of such technologies. These technologies allow China to export tools of censorship and surveillance. They also provide China with tools to influence states and to potentially gain access to their national information and data. (Markey, 2020 )

Despite its fanfare and high expectations, the CPEC has not turned out to be as advantageous for Pakistan as originally had been hoped. One issue with the CPEC is that most of the contracts have been concluded without adequate transparency. There is lack of detail on everything from the scale of individual investments, the size of their debts, the impact of these investments on the Pakistani economy, and the level of corruption that each of these investments generate. For instance, the Governor of Pakistan’s Central Bank has stated publicly that he had no clear idea how much of the CPEC projects were being financed by debt, by equity or by in kind; what is certain is Chinese investment terms have been far from concessional. This lack of clarity has been magnified by the fact that Pakistan has been negotiating its CPEC deals from a position of weakness as Pakistan has few other foreign direct investment sources, and many infrastructure and other needs. Poor transparency has also raised concerns that Pakistan might find itself in a debt trap.

Another issue for Pakistan regarding the CPEC is that the economic benefits of the CPEC have not been spread equally throughout Pakistan but have been concentrated in Punjab province. Punjab is Pakistan’s largest, wealthiest, and most stable province, making it the easiest place for CPEC projects to build on existing infrastructure. This lack of geographical distribution is causing opposition to the initiative in the unfavored provinces and territories, particularly in Baluchistan and Gilgit-Baltistan. For instance, despite the terminus of the CPEC being located Baluchistan’s Gwadar Port, little economic benefit from the CPEC appears to be trickling down to the province. Instead, Baluch groups are experiencing a loss of the land in their traditional tribal area, reduced autonomy, and blocked access to traditional fishing beds.

Karachi – Pakistan’s Financial Center

Another concern is that CPEC projects our being primarily funded by Chinese loans which primarily benefit Chinese companies who earn and often expatriate most of the profits generated by the work. In the best-case scenario, Chinese companies profit by expanding into neighboring markets. If the loans eventually prove untenable or are only partially repaid, then China still benefits as its efforts have served to subsidize its own firms, even if at a loss. Ultimately, China conceived the Belt and Road initiative as much from a position of weakness as from strength. Facing massive overcapacity in many of its basic industries, China is now exporting that capacity abroad.

Many in the Pakistani business community – already been hard-hit by the 2007 Free Trade Agreement – do not want to be disadvantaged again by the CPEC. Pakistani businessman worry that a limited elite will benefit from privilege relationships with Chinese companies, while those on the outside will suffer disproportionately. The Port of Karachi, for instance, sees the Chinese port of Gwadar as a direct competitive challenge; Karachi Port is currently operating far below capacity and would prefer additional infrastructure investments to come its way as opposed to being channeled through the Gwadar Port.

Pakistani business and government officials are also concerned that the CPEC could install a potentially unwelcome Chinese presence in virtually every sector of the Pakistani economy. Pakistani citizens and businessmen have expressed concern about the potential influx of Chinese workers, about their land being appropriated, and about the infiltration of Chinese cultural norms that are inconsistent with Pakistan’s more conservative Islamic culture. Although exact figures are unavailable, it is estimated that approximately 40,000-70,000 Chinese workers are now operating in Pakistan. The Pakistani military has created a special Chinese Pakistan Economic Corridor division of over 15,000 troops to provide these workers with additional protection.

Gwadar Port

The Gwadar port is located in the Balochistan province of Pakistan. This port is strategically located a mere 76 nautical miles from Chabahar, an Iranian free port located on the coast of the Gulf of Oman. India has invested significant resources in developing it, in part to counter Chinese presence at Gwadar. To further connect Chabahar with the Middle East, India was planning to invest in a $400 million railway system to link Chabahar to Zahedan, a city in Iran close to the border with Afghanistan (Baptista, 2020). Recently, however, Iran has replaced Indian investment in the railway with Chinese investment, which hinders India’s efforts to restrict Chinese geopolitical maneuvering. China efforts could result in India being encircled by China-friendly countries, hampering India’s efforts to develop influence in the region. (Jafari, 2020)

Chabahar Port

Like the Karakoram Highway, Gwadar Port is not interesting as an economic proposition alone. Instead both the port and highway are most interesting for their geopolitical value. For Pakistan, the Gwadar Port expands Pakistani governmental reach into its frontier regions, consolidating its presence in traditional Baluchistan tribal land. Baloch militants have argued that China is facilitating these efforts by exporting to Pakistan technological tools of repression.

The Gwadar Port also provides it with a second naval base. For China, it gives China’s western regions access to the Indian Ocean and its global trade networks. It will also likely give the Chinese navy a permanent base on one of the world’s largest and most strategic deep-water ports. A permanent base would allow it to resupply and undertake repairs both of its ships and the weapons systems that the ships carry away from the Chinese mainland.

A view of the Gwadar Promontory and Isthmus

Not only is China financing the development of the port, but it is also financing all the infrastructure that the port requires including housing, hotels, warehousing facilities, roads, an airport, a free-trade zone and freshwater treatment and water supply. Creating water infrastructure is particularly important as the area has been plagued by shortages.

The Baluchistan people have been against the project. Besides the port and infrastructure encroaching on traditional tribal lands, the Baluchistan people fear that most of the economic benefits of the port will go to people outside the province. Because of China’s investments, in 2017, Pakistan’s Federal Minister for Ports and Fisheries estimated that 91% of the profits from Gwadar Port would stream to China over the next 40 years. The other 9% will likely go to Pakistan’s federal government, leaving provincial and local authorities with little benefit. The port is expected to bring a large influx of people into the region. Once fully developed, Gwadar Port and city may be home to as many as 2 million people. Already, prime real estate near the port has been acquired by private investors in the Pakistani Navy, while traditional fishing communities have been forcibly relocated. So far, most new jobs have gone to non-Baluchistan peoples.

Pakistan, China and the Uighurs

Xinjiang Uyghur Autonomous Region is China’s only Muslim-majority province. In 2017, it is estimated that the Uyghurs accounted for only 46% of the 22 million population while ethnic Han represent at least 40% of the total. Xinjiang is also China’s largest province, covering more than a sixth of Chinese territory. Xinjiang is resource rich containing substantial deposits of natural gas, oil, and coal. The province is also home to important military sites including the Lop Nur nuclear weapons testing facility.

Uyghur men in Kashgar

As China expands its Belt and Road Initiative through Pakistan, Central Asia, and the Middle East, China has concerns that these connections will make it vulnerable to importing radical Muslim movements into the province that might encourage its ethnic Uyghurs to agitate for separatism. As a result, China has instigated a large-scale reeducation camp system designed to replace Uyghur Muslim proclivities with outlooks that align more closely with Chinese state doctrine. China has overlaid this reeducation policy with systematic technological and police surveillance.

Abroad, China has pressed Central Asia governments and Pakistan to root out terrorism, separatism, and religious extremism. With Pakistan specifically, China is using its influence in the country to eradicate any radical elements that might try to agitate in Xinjiang. The Pakistani military has used its influence, for instance, to dissuade any state-sponsored militant groups from focusing their efforts toward China and has shared intelligence with China regarding militant activities. China has supported Pakistani intelligence efforts by providing funds and small arms to militant groups who do not advocate on behalf of the Uyghurs in a “don’t-poke-us-and-we-won’t-stomp-on-you” arrangement. To date, Chinese efforts have been largely successful at both controlling its Muslims at home and preventing the import of radicalism from abroad.

Independently, China has increased its monitoring of Uyghurs in Pakistan likely numbering no more than 40 for 50 militants. Given the weakened state of the Uyghur remnants in Pakistan, there has been some question as to why the Pakistani Army does not move to eliminate the Pakistani Uyghurs completely. One theory is that their presence on Pakistani soil makes the Pakistani military more useful to China than it would be if all the Pakistani Uighurs were assassinated.

Pakistani soldier

While China is appreciative of the Pakistani military’s efforts to support China’s control of its Muslim population, China is concerned, however, about the growing Islamization of the Pakistani Army. Specifically, China is observing instances where the Pakistani military has become increasingly involved with radical Islamist militant agendas and where the military is more actively using such militants to achieve its own political and other goals. In theory, if not always in practice, these militant proxies offer Pakistan the benefit of plausible deniability. This reduces the cost to Pakistan of militant violence and diminishes the risk of escalation, at least in comparison to conventional military operations. China expects the Pakistani military to keep China off the terrorist target list, and to keep its citizens safe within Pakistani borders. To the extent that Pakistan cannot fulfill this role, China expects to be able to deploy its own military in Pakistan to protect its citizens just as it does in several places in Africa.

Future Trends

China and Pakistan will continue to deepen their military, economic and political alliance in the future. The Sino-Pakistani military relationship is the strongest pillar to their alliance. Going forward, this relationship will continue to deepen through the Chinese failed to Pakistan of weapons and technology, through shared intelligence and through joint military exercises.

Economically, the China-Pakistan Economic Corridor will drive deeper economic ties between the two countries. That said, both countries have expressed reservations about the CPEC. From China’s perspective, there is concern about Pakistan’s ability to repay China’s investments financing. From Pakistan’s perspective, there is concern about how much Pakistan wants China’s involvement in every aspect of its economy. Many Pakistani businessmen have already seen how the free trade agreement between the two countries flooded Pakistani markets with goods at prices that make Pakistani-produced goods untenable; they also see how many of the profits generated by CPEC are being exported back to China. Pakistani economic leaders also worried that the lack of transparency regarding CPEC deals risks overwhelming the country with debt. Despite these concerns, the benefits of CPEC to both countries will outweigh these risks. While CPEC investments will not roll out as rapidly as originally projected, it is expected that China will continue to heavily invest Pakistan going forward.

Economically, the China-Pakistan Economic Corridor will drive deeper economic ties between the two countries. That said, both countries have expressed reservations about the CPEC. From China’s perspective, there is concern about Pakistan’s ability to repay China’s investments financing. From Pakistan’s perspective, there is concern about how much Pakistan wants China’s involvement in every aspect of its economy. Many Pakistani businessmen have already seen how the free trade agreement between the two countries flooded Pakistani markets with goods at prices that make Pakistani-produced goods untenable; they also see how many of the profits generated by CPEC are being exported back to China. Pakistani economic leaders also worried that the lack of transparency regarding CPEC deals risks overwhelming the country with debt. Despite these concerns, the benefits of CPEC to both countries will outweigh these risks. While CPEC investments will not roll out as rapidly as originally projected, it is expected that China will continue to heavily invest Pakistan going forward.

Along with its infrastructure investments in Pakistan, China is also expected to export surveillance and other technologies. These technologies are expected to increase the repression of civil society within Pakistan. China will also increasingly export media content to the country in order that Pakistan and China can create a narrative within Pakistan that highlights the benefits of their relationship to the Pakistani populace.

Politically, both countries will continue to support each other’s geopolitical goals. The most important geopolitical goal that both countries share is their desire to mitigate the rise of India. These mitigation efforts will involve everything from jointly working to push back on Indian efforts to extend its control in Kashmir to thwarting India’s efforts to expand its presence in the Indian Ocean and abroad.

")

China is answering these challenges by significantly investing in agricultural technologies including artificial intelligence, big data, robotics, and automation. Not only will these technologies help improve the efficiency and sustainability of China’s agricultural market, but they also represent a big and rapidly growing global business. The market for global agricultural robots, for instance, is projected to exceed $20 billion by the end of 2025, with growth in precision agriculture as a major driver. Artificial intelligence, automation, big data, and robotics are expected to find applications in everything from herding and fish farming to planting and harvesting. Other uses include seeding, irrigation, water leak detection, fertilizing, crop weeding, spraying, crop monitoring and analysis, disease and pest identification and eradication, thinning and pruning, and tracking the growth of plants. In addition to robotics, drones are also increasingly being used to monitor crops, conduct field analysis, manage livestock, plan interrogation and crop spraying. Drones aid farmers to see the big picture of their farmland and to make educated decisions that help to maximize crop yields.

China is answering these challenges by significantly investing in agricultural technologies including artificial intelligence, big data, robotics, and automation. Not only will these technologies help improve the efficiency and sustainability of China’s agricultural market, but they also represent a big and rapidly growing global business. The market for global agricultural robots, for instance, is projected to exceed $20 billion by the end of 2025, with growth in precision agriculture as a major driver. Artificial intelligence, automation, big data, and robotics are expected to find applications in everything from herding and fish farming to planting and harvesting. Other uses include seeding, irrigation, water leak detection, fertilizing, crop weeding, spraying, crop monitoring and analysis, disease and pest identification and eradication, thinning and pruning, and tracking the growth of plants. In addition to robotics, drones are also increasingly being used to monitor crops, conduct field analysis, manage livestock, plan interrogation and crop spraying. Drones aid farmers to see the big picture of their farmland and to make educated decisions that help to maximize crop yields.