Introduction

China’s enormous population is one of the country’s most defining features. With the largest population in the world, almost one-fifth of the global total, it factors into nearly every significant issue facing the country including employment, consumption, the environment, and migration. In the 1970s, faced with the prospect of its population outstripping its economic and agricultural output, Beijing reversed early Maoist policies encouraging population growth. China’s 1970s aggressive fertility education programs and its 1980 “One-Child Policy” succeeded in reducing births per woman from their peak of 5.8 at the beginning of the 1970s to approximately 1.6 in 2019. The success of China’s population control policies has had unexpected disadvantages including a male/female sex imbalance, a rapidly aging population and a shrinking labor force. In 2016, such difficulties caused China to change the One-Child Policy to a Two-Child Policy. Nevertheless, despite policy changes and China’s declining numbers, China’s large population still poses significant challenges for the country.

Global Population Trends

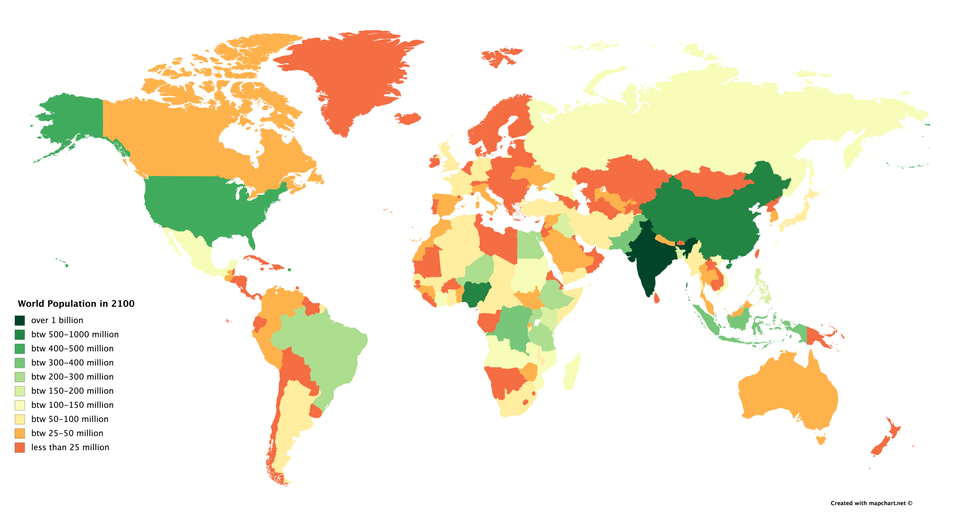

Understanding global population trends brings context to China’s individual demographic numbers. According to the United Nations 2019 Population Report, the global population is expected to rise from 7.7 billion in 2019 to approximately 10.9-11.2 billion in 2100. By then, approximately 81% of the world’s population will be living in Africa and Asia.

|

UN Population Statistics – Geographical Regions |

|

|

|

|

|

|

|

|

|

|

|

|

| Regions |

2019 |

2019 |

2030 |

2030 |

2050 |

2050 |

2100 |

2100 |

| World |

7,713 |

|

8,548 |

|

9,735 |

|

10,875 |

|

| Sub-Saharan Africa |

1,066 |

14% |

1,400 |

16% |

2,118 |

22% |

3,775 |

35% |

| Northern Africa and Western Asia |

517 |

7% |

609 |

7% |

754 |

8% |

924 |

8% |

| Central and Southern Asia |

1,991 |

26% |

2,227 |

26% |

2,496 |

26% |

2,334 |

21% |

| Eastern and Southeastern Asia |

2,335 |

30% |

2,427 |

28% |

2,411 |

25% |

1,967 |

18% |

| Latin America and the Caribbean |

648 |

8% |

706 |

8% |

762 |

8% |

680 |

6% |

| Australia/ New Zealand |

30 |

0.4% |

33 |

0.4% |

38 |

0.4% |

49 |

0.5% |

| Oceania |

12 |

0.2% |

15 |

0.2% |

19 |

0.2% |

26 |

0.2% |

| Europe and North America |

1,114 |

14% |

1,132 |

13% |

1,136 |

12% |

1,120 |

10% |

Sub-Saharan Africa will experience the greatest growth. As a proportion of global population, between 2019 and 2100, the region will increase from 14% of the total or 1.1 billion people to 35% or 3.8 billion. Between 2019 and 2050, the world’s 47 least developed countries will grow the fastest, with many countries doubling in size. Of the 2019-2050 expected increase of 2.1 billion people, half the increase is projected to be driven by just nine countries: India, Nigeria, the Democratic Republic of the Congo, Pakistan, Ethiopia, the United Republic of Tanzania, the United States, Uganda and Indonesia.

As a proportion of the global total, the rest of the world will experience flat or decreasing population levels. Flat-growth regions include North Africa and West Asia which are projected to grow from 7%-8% or 527 to 924 million people between 2019 and 2100. Oceania will stay steady at .2% or 12 to 26 million people. Australia and New Zealand will grow from .4%-.5% or 30 to 49 million people.

Those with shrinking populations between 2019 and 2020 include Europe and North America which will decline from 14% to 10% of the global total, holding steady at approximately 1.1 billion. Latin America and the Caribbean will drop from 8% or 648 million to 6% or 680 million people. Central and Southern Asia will drop from 26% or 2.0 billion to 21% or 2.3 billion people. Eastern and Southeastern Asia will decrease from 30% or 2.3 billion to 18% or 2.0 billion people. In Europe, the population is expected to peak in 2030 at 510 million and then decrease to 465 million by 2100.

In 2019, China at 1.4 billion and India at 1.3 billion accounted for 37% of global population. In 2100, China at 1.1 billion and India at 1.45 billion will drop to 23% of the global total. By 2024, India is forecasted to overtake China to become the world’s most populous country.

Rapid worldwide urbanization is a big driver in the decreasing fertility rates seen in most regions. In 2019, approximately 55% of people worldwide lived in cities. By 2050, the percentage increases to 68%, and by 2100 to 84%. Urbanization places downward pressure on birth rates because children that were once useful as farm labor become burdens in cities where they need to be educated and trained in order to be economically productive. Additionally, urban women have better access to education, healthcare and work opportunities, all of which make them less inclined to have large families.

Worldwide, in most countries where populations are declining, people are also quickly aging. In 2100, the number of people 60 years or over is expected to grow to 28% of the total population, from 1.0 billion to 3.1 billion people. The number aged 80 or over will increase to 8%, from approximately .1 billion to .9 billion people. Correspondingly, the global fertility rate is expected to drop from 2.5 in 2019 to 1.9 births in 2100. The global fertility rate is expected to fall below the replacement fertility rate by the year 2070, with the replacement fertility rate being the level of birth that each female is required to have to keep up with the population size. This aging population is expected to affect everything from economic demand to social safety nets.

Emigration and immigration are also impacting population levels in some countries. Countries such as Bangladesh, Nepal, the Philippines, Syria, Venezuela, and Myanmar have seen over 1 million of its citizens emigrate since 2010, either in search of work opportunities or to escape war or internal domestic conflict. Conversely, since 2010, over 36 countries have welcomed over 200,000 immigrants.

China’s Population Trends

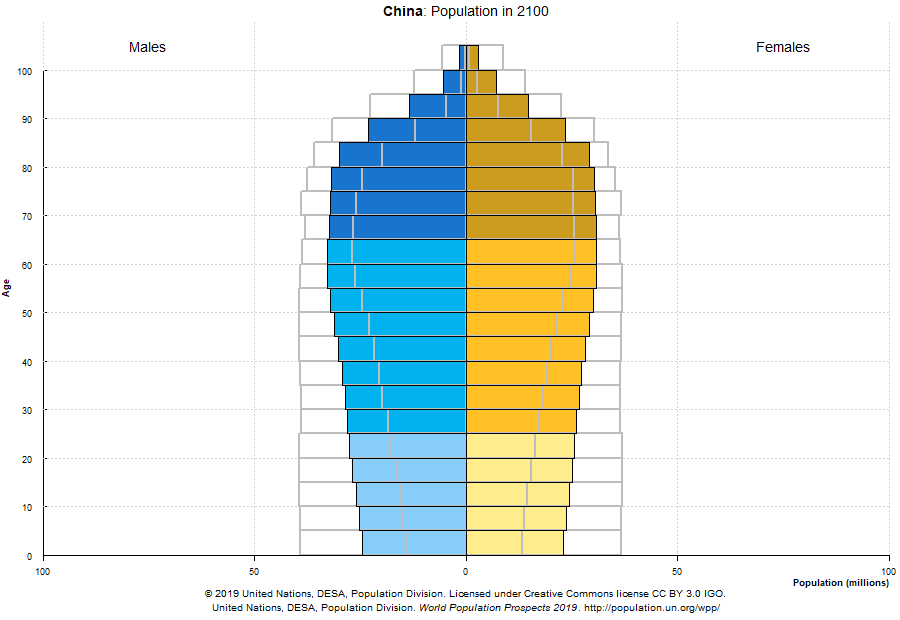

China is experiencing rapid demographic change that mirrors many global trends. As is happening in many East Asian countries, China’s population is declining both in absolute numbers and as a percentage of the world total. According to UN statistics, in 2019, China’s population was approximately 1.434 billion people or 19% of the global total. By 2035, China’s population is expected to peak at 1.461 billion people or 16%. By 2050 and 2100, China’s population will reduce to 1.402 billion or 14%. and 1.064 billion or 10% respectively. Currently, the fertility rate of China is 1.55 births per woman.

China’s population faces a significant sex imbalance. In 2019, there were approximately 37 million additional males to females, with males accounting for 51.30% of the total. While the absolute number of additional males is forecasted to decrease, as a percentage of China’s total population, males will continue to outnumber females through 2100. By 2050, for instance, China will have 24 million more males than females, with males accounting for 50.87%. By 2100, males still exceed females by 25 million or 51.15% of the total.

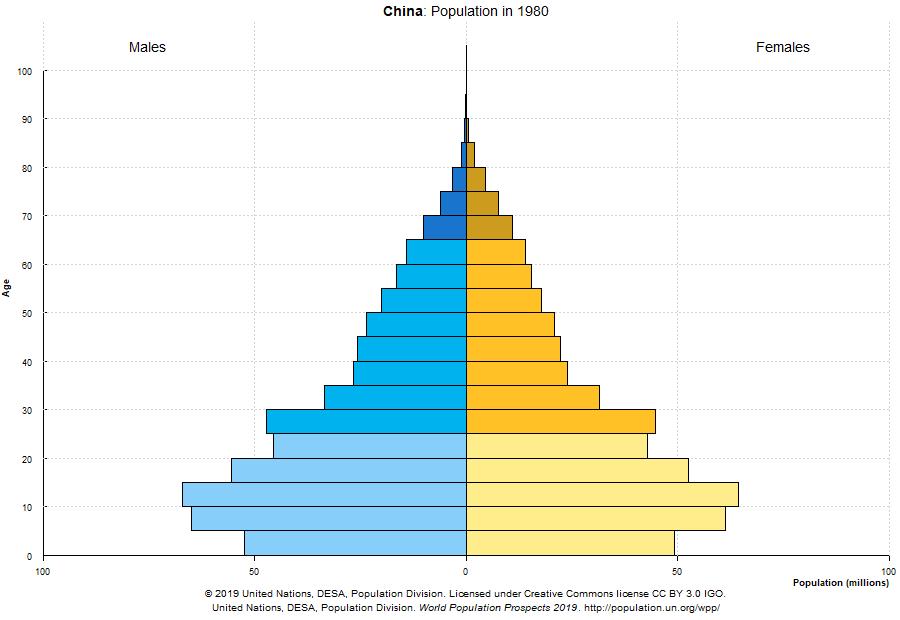

China’s population is also aging rapidly. In 1980, China’s population aged 50+ was 14% of the total, with people aged 75+ accounting for just 1% of those in the 50+ category. In 2019, China’s population aged 50+ increased to 32%, with people aged 75+ accounting for 3% of 50+ category total. By 2050, China’s population 50+ surpasses 47%, with 14.1% of this group aged 75+. By 2100, this group exceeds 49%, with 20% of this group being 75 years or older.

| UN Population Statistics – China – By Age Category |

|

|

|

|

|

|

|

| Age Demographics |

1980 |

2020 |

2050 |

2100 |

| 0-14 |

35.9% |

17.7% |

14.1% |

13.8% |

| 15-49 |

49.7% |

49.5% |

38.7% |

36.6% |

| 50+ |

14.4% |

32.8% |

47.2% |

49.6% |

| 75+ |

1.2% |

3.7% |

14.1% |

20.0% |

China’s Population Post-1949

For the best part of two millennia, China had been the most world’s populous country. In the early 1800s, for instance, one-third of the world population was Chinese. While still having the world’s largest population in 1950, between 1850 and 1950, high death rates caused by disease, crop failure, natural disasters, and war restrained China’s population growth to 0.3% per year. In 1949, after the Chinese Communist Party (CCP) victory in the Chinese Civil War, early CCP policies led to improvements in nutrition, sanitation and increased access to healthcare. Chinese mortality rates, especially those of infants, plummeted and the population began to grow rapidly. Initially, China’s leader, Mao Zedong, considered a large and rapidly growing population to be a positive asset. More people meant more workers to aid in economic development. More people meant more soldiers to ensure Communist domestic control, to secure China’s international borders and to prosecute war. Mao believed that Malthusian theory –the principle that exponential population growth can lead to an inability to feed the population – was a capitalist paradigm that did not apply to Marxist production methods where more people created more economic output.

As a result, China’s population continued the tradition of seeking as many sons as possible. According to U.N. statistics, between 1950 and 1980, China’s population almost doubled, increasing from 554 million to just over 1 billion. Officials in China were aware of China’s exploding population in the decades after 1949. Yet, any talk of population control or family planning was labeled as defeatist.

By the end of the 1960s, concerns regarding China’s exploding population began to be more discussed more openly. In 1970, Beijing decided to implement a voluntary birth control system. The government made contraceptives more widely available and educated the public on new government family planning policies with slogans promoting “later marriages, longer birth intervals and fewer children”. The program was largely successful. China’s total fertility rate, which measures the average number of births per woman, plummeted from 5.8 in 1970 to 2.7 in 1978. A 1980 study, undertaken to determine what would be China’s ideal population in 2080, assuming significant modernization and economic growth, concluded that the optimum level was between 650 and 700 million. As China’s population in 1980 had already exceeded 1 billion citizens, the government decided to implement more draconian population control measures.

The ‘One-Child’ Policy

In September 1980, China launched the One-Child Policy. Family planning was written into the constitution two years later. The policy was not implemented uniformly across the country. Most ethnic minorities were permitted to have two children and many Han living in rural areas could have a second child if the first child was a girl. Additionally, parents whose first child was disabled could have a second child. Nevertheless, by the late 1990s, China’s total fertility rate fell to between 1·5 and 1·7 where it has remained.

The One-Child Policy was implemented relatively easily in the cities, where both spouses often worked and where living conditions were cramped. Resistance in the countryside was greater. The rural desire for larger families and many sons has been deeply rooted, not least because more hands make agricultural work easier for all. In general, there has been a high correlation between higher income and the willingness to accept the One-Child Policy.

One result of the policy has been greater incidences of forced sterilizations and abortions (Short, 2000). More commonly, couples defying the One-Child Policy were subject to fines, loss of jobs, reduced wages, loss of work unit benefits or, in some cases, loss of bonuses for the entire workgroup. In some areas, relatively wealthy families who worked in the private sector were able to pay the fines imposed. Those working in the public sector did not have this freedom as a second child usually meant a loss of employment. Others did not report females at birth. Unregistered girls were at risk of losing access to many legal benefits, including education and other forms of social welfare. It is not clear exactly how many unregistered girls were born in China since 1980, but research by John Jay Kennedy at the University of Kansas estimates that 10 million undocumented girls were born from 1980-2010.

The One-Child Policy has also led to an imbalance in the male/female sex ratio. In 2019, there was an estimated 37 million more men than women. Termed “Bare Branches” in China, these men are statistically unlikely to find partners in a society where universal marriage is the norm; 99.5% of Chinese women and 97% of all Chinese men marry. Men who do marry tend to be those with higher incomes, better educations and higher-value assets, including an apartment, house or car. Surplus men tend to be concentrated in rural villages that are poverty stricken. Those men unable to find wives statistically are more likely to engage in prostitution, social unrest and crime.

A benefit of this imbalance has been a greater trend toward gender equality. Historically, Chinese parents devoted relatively few resources to their daughters. A 2018 study by Yi Zeng and Therese Hesketh found that without brothers with which to compete, there were no significant differences between single-girl and single-boy families in terms of a family’s investment in and expectation for health and education outcomes. In 2018, women made up 52% of undergraduates and 48% of postgraduates. Having less children has also improved women’s access to well-paid work and career advancement. In 2018, it is estimated that as many as 25% of CEOs of medium and large Chinese companies are women.

China’s Rapidly Aging Population

The One-Child Policy has also contributed to China’s rapidly aging population. In 1980, China’s population aged 50+ was 14% of the total, with people aged 75+ accounting for just 1% of those in the 50+ category. In 2019, China’s population aged 50+ increased to 32%, with people aged 75+ accounting for 3% of 50+ category total. By 2050, China’s population 50+ surpasses 47%, with 14.1% of this group aged 75+. By 2100, this group exceeds 49%, with 20% of this group being 75 years or older.

This rapidly aging population will place a great burden on the younger segments of society as the elderly dependency ratio increases sharply. The elderly dependency ratio is defined as the number of people aged 65+ years divided by number of working-age people aged 18–64 years. As dictated both by Chinese culture and by Chinese law, Chinese children are obliged to care for their retired parents. The strain of caring for the elderly is expected to be more significant in the countryside. The elderly in rural areas generally enjoy a less robust social safety net compared to those living in in urban areas. On average, rural lifetime incomes are less as well, leading to lower retirement savings. Rural elderly are also more vulnerable to living alone, as many rural children have migrated to cities to find work. Rural empty-nesters, especially those living alone, are more likely to suffer mental health, financial and other problems.

The Two-Child Policy

Because of these negative population trends, in January 2016, China’s One-Child Policy changed to a Two-Child Policy. For the first time in 36 years, no one in China is limited to having just one child. The policy was aimed at the 90 million women within the reproductive age that presently had a child and now would be permitted to have a second child. In some provinces, these policies have been supplemented by incentives such as encouraging employers to provide more services for families, to lengthen maternity leave, to offer aid to women returning to work after birth and to grant tax incentives, housing benefits and education cost deductions. Some provinces are making abortions harder to obtain and using courts to discourage couples from accessing divorce services.

Despite these efforts, the significant socioeconomic changes that occurred since the onset of the One-Child Policy have caused China to transform into a low fertility culture. These changes are consistent with the pattern countries follow as they become more developed. Studies have indicated that most Chinese rural women want 1 to 2 children compared to greater than 5 children desired in the 1970s. Most urban women continue to want only one child. Urban women’s list of reasons for their one child preference include the high cost of raising and educating children, the negative effect a larger family would have on her family’s lifestyle and her individual liberties, the greater strain more children would place on family income and the impact more children might have on a her career. Factors affecting rural fertility include a woman’s marriage age, the cost of children, income forgone for having children and the social security benefits available. The Two-Child Policy is therefore unlikely to unleash a baby boom, but rather should cause a modest increase in fertility. That said, many of the negative effects of the one-child policy are likely to disappear. These include forced abortions and sterilizations, female infanticide or abandonment and unregistered girls at birth.

The Changing Structure of the Labor Force

Since 1980, the age structure of China’s population has provided China with an enormous competitive economic advantage. Specifically, since 1980, China’s population has been both young and relatively free of dependents, whether they are children or elderly parents needing care. In 1980, for example, 85% of its population was aged 49 years or younger, with 50% of that population falling into the 15-49 year working age bracket. In 2019, 50% of China’s population was still aged 15-49, but its total population aged 49 years or younger has decreased from 85% to 67%. China’s current low dependency rate derives from the fact that Chinese ‘baby boomers’ born in the 1960s after the Great Leap Forward, and their children born in the 1980s, are now of working age. During the 1980s, China’s working age population increased 2.5% annually; this increase, coupled with high rural-to-urban migration, meant that the overall urban labor force has grown at about 4% per year between 1978 and 2010. It is expected that between 2010-2027, the number of Chinese workers will level off and then begin to drop approximately .5% per year. This decline will mirror a rising dependency rate as the ratio of producers to total population decreases.

The historically low dependency rate has created a “demographic dividend” for China. The demographic dividend is the economic growth potential that can result from shifts in a population’s age structure, mainly when the share of the working-age population is larger than the non-working-age share of the population. China’s low dependency rate since 1980 has also helped drive high savings rates, as individuals tend to save when they work and then spend their savings upon retiring. This savings has provided the Chinese economy with significant investment capital which in turn has led to the creation of more jobs. China’s young, unencumbered population has also benefited China economically, as it has been more adaptable to the rapid social and economic changes that have attended China’s transition to a market economy.

In 1978, 99% of these Chinese laborers worked in government-owned enterprises. In 2014, Chinese workers are employed by a more diversified set of companies in terms of ownership structure. While 25% of urban workers still work for the government or government-controlled entities including collectives and state-owned enterprises, 43% work for privately-owned firms, and 32% are self-employed or work in the informal economy.

Going forward, the growth of China’s labor force will slow as the last baby boom cohorts are absorbed. According to UN population calculations, by 2050, 47% of Chinese people will be over 50 years compared to 33% in 2019. Between 2020 and 2050, Chinese workers – those aged between 15-59 years – will decrease by over 200 million people, an average of 7 million people annually.

To offset its diminishing labor pool, China has many tools at its disposal. A start has been the easing of the One-Child Policy. Although it is too early to measure accurately the impact of the Two-Child Policy, early research indicates that the population bump will be relatively small. Population is now expected to peak at 1·45 billion in 2029 compared with a peak of 1·4 billion in 2023. In addition to implementing the Two-Child Policy, China can continue to modernize and mechanize China’s farming. Chinese fields typically average 2.5 acres, one of the smallest averages in the world. Increasing farm size will facilitate the use of modern farming technologies. Both will create opportunities for the remaining 27% of Chinese workers still employed in agriculture to migrate to the industrial workforce. Automation and robotics can also offset labor declines and increase labor productivity. Overall, Chinese labor productivity is likely to rise in coming decades because incoming labor cohorts are more educated than their parents. China can also extend the retirement age. Currently, men retire at 60 years and women retire at 55 years.

Urbanization

Rapid urbanization has accompanied China’s economic development. Historically, China has been a country of farmers. In 1950, when the Communists took control, only about 10% of the country lived in cities. Early Chinese Communists policies reinforced this rural population bias by creating what amounted to a two-tier economic system. Chinese urban citizens, enmeshed in danweis or urban work units, enjoyed social benefits and welfare entitlements not available to farmers housed in the rural collectives. This inequality was designed to generate rapid industrialization. Rural China was to provide low-cost food and other agricultural products to city workers who used the savings from these low-cost goods to invest in and build China’s factories.

In order to prevent peasants from migrating to seek better work and greater benefits, the household registration system (hukou) was developed which was accompanied by a system of vouchers which were required to acquire food and clothing. By the early 1960s, it became almost impossible for rural workers to obtain an urban hukou, and rural to urban migration was almost completely halted. Indeed, internal migration between 1964 and 1980 was almost exclusively from the city to the countryside as happened during the Cultural Revolution when approximately 17 million middle school graduates were sent to the country to “learn from the peasants” and as happened when workers were sent to develop industry in Western China. As a result of these measures, by 1978, only 17.92% of Chinese lived in cities.

After 1980, China began to rapidly urbanize as its economy expanded. According to World Bank statistics, in 2018, approximately 59% of Chinese live in cities or almost 850 million people. By 2030, it is estimated that 70% or one billion of Chinese will be urban residents. Some urban growth has occurred by reclassifying rural areas to urban areas, but most of the growth in the urban residential rate represents real rural to urban migration. Currently, China has 65 cities over 1 million people, and 15 cities with population larger than 10 million. According to World Atlas statistics, in 2019, Ghangzhou was China’s largest city with 44.2 million people followed by Shanghai with 36 million people.

Internal Migration and the Hukou System

To control its large population, in the 1950s, China implemented the household registration or hukou system. This system effectively tied people to the place in which their Hukou registration card was issued. Children inherited their hukou status from their parents. Besides controlling internal migration, the hukou system controlled the internal distribution of resources such as food and clothing. The hukou system prioritized urban workers over rural workers. Non-agricultural and urban residents were granted significantly better benefits including superior employment opportunities, free education for their children, free and more-advanced medical care, subsidized housing and retirement pensions. By contrast, rural residents received few benefits and were also required to sell their produce to the government at discounted rates in order to finance urban subsidies. Inferior benefits and poorer educational and work opportunities has meant that rural residents have experienced significantly less upward mobility when compared to urban inhabitants. Chinese police have also used hukou registration to more closely watch problematic citizens such as political activists or convicted criminals.

In the 1980s, agricultural reforms led to surplus labor at a time when industrial economic reforms caused the demand for urban workers to increase. As a result, China began to cautiously modify Hukou restrictions. In 1984, for instance, China created the “self-supplied food grain” hukou which allowed rural residents to live in market towns if they had local employment, housing and food. In 1992, wealthy and educated individuals could earn urban residency under the “blue stamp” hukou designation if they had significant funds to invest in urban areas.

In addition to workers migrating with new Hukou status, millions of rural Chinese have also traveled to cities illegally. Illegal migration has been facilitated by the steady reduction in the use of Hukou ration vouchers, meaning that unregistered migrants have been able to purchase food and clothing once they have reached the city. According to Chinese labor bulletin statistics, in 2018, approximately 30% of the workforce or 288 million workers are currently part of what is termed China’s floating population. Most of these migrants live on the periphery of cities often in substandard housing. They work long hours and expect to return home once they have met their financial objectives. Migrant workers tend to take jobs that urban residents are either unable or unwilling to do. Male migrants, for instance, dominate employment in sectors such as construction, while females work in textile and other factories were work is strenuous and often dull.

Migrants lack channels into urban society including access to education, housing and social services that go with full urban citizenship. In comparison to urban residents, rural people have lower educational levels and are equipped with less capital. They also suffer the economic and emotional impact of remoteness and they endure incomplete markets for many needed resources. Without access to education, many migrants leave their children behind with family members in the countryside. Typical work schedules mean that visits home occur infrequently, often just once a year.

As its floating population has grown, China has continued to address migrant disadvantages through gradual modifications of registration requirements. This process has been implemented in starts and stops. Reforms began first in small towns and cities. Where migrants can demonstrate extended residence, secure housing and steady income, it has become easier to transfer their hukou registration. Since 2001, larger cities have also begun some limited easing of hukou restrictions. In 2014, the national government has reiterated its pledge to continue to gradually eliminate the urban registration system. Cities and towns with populations under 1 million people are now required to eliminate restrictions entirely and promptly. Cities of 1- 5 million people have been given more open-ended deadlines to meet hukou reform goals. Cities with populations greater than 5 million people can continue to restrict access to permanent registration.

Where local cities have tried to push back on allowing more migrants to formally register, they have done so by defining criteria strictly. For instance, many cities have interpreted the steady source of income criteria in a way that excludes the unskilled jobs that employ many migrants. Other cities have required educational or wealth criteria that are often not met by many in China’s floating population.

These criteria effectively keep in place the significant barriers stopping low-wage earners from being upwardly mobile. They have minimized the impact of the reform by limiting its benefits to a small part of the migrant population. Cities often support these barriers because adding migrants to the formal registration system generates meaningful educational, healthcare, housing and other social costs. Barriers also entrench urban privileges from which city officials themselves benefit, and act to keep urban populations loyal. Hukou restrictions have prioritized the economic growth of China’s urban areas over rural areas. Rural migrants subsidize urban industrial growth by providing low-cost, benefit-free labor. Hukou allows urban environments to control the numbers of such workers by preserving their option to remove illegal workers from the city when their labor is no longer beneficial. One way that local Chinese governments have tried to mask the existence of continuing barriers is by eliminating hukou labels – rural, urban, blue stamp, etc. – while keeping in place the criteria that made the labels relevant in the first place. That said, overall, the trend is that household registration restrictions are continuing to ease even if progress is slow.

Additionally, other migrant-beneficial reforms are being promoted. For instance, there have been efforts made to rein in detrimental police practices including coercive custody and repatriation, dragnet sweeps and extortion. Other directives have stipulated that more effort should be made to educate the children of migrants working within local jurisdictions. Some local governments have tried to skirt this requirement by making education available only to those migrants who have no family members still residing in their hukou registration jurisdiction. Where education is provided, migrants often are required to pay additional fees not required by local hukou holders. These fees often represent a significant percentage of the migrant’s annual income and represent an additional income source for schools. In order to prevent the loss of these additional school fees, the establishment of private migrant schools has often been strongly discouraged.

Limited educational access is also at play when trying to gain access to colleges and universities. Competition for acceptance to local universities is fierce even if students are legal. Non-registered students are often required to achieve significantly higher test results compared to registered students when vying for the same place. By limiting labor mobility, China’s amplifies the income disparity between urban and rural residents, creating a hereditary economic barrier.

Chinese Diaspora

Chinese Diaspora or Overseas Chinese are people of Chinese birth or Chinese descent currently living outside the People’s Republic of China and the Republic of China (Taiwan). Today there are an estimated 40 million overseas Chinese living in 148 countries around the world. The majority lives in Southeast Asia. Ethnic Chinese constitute approximately 74% of the Singaporean population as well as significant minority populations in Indonesia, Malaysia, Thailand, the Philippines and Vietnam. Historically, most came from the southern coastal provinces of Guangdong, Fujian and Hainan. In each geographical region where Chinese reside, many of the Chinese diaspora have kept their languages and cultural identity while integrating to varying degrees into their host country.

Map of Chinese Migration 1800-1949

Chinese migration came in four waves. According to research by Poston and Wong, the first wave was characterized by merchants and traders who emigrated to create businesses abroad. The more successful their businesses, the more likely these migrants were to preserve their Chinese attributes and their connections with China. Most of these merchant migrants traveled to Asian countries, particularly to Southeast Asia before 1850. A second wave of migration occurred between approximately 1840 and 1920 when Chinese immigrated to the Americas and Australia to work as cooks, miners, laundry men and railway construction workers. Most of these immigrants were male, of peasant origin and many returned to China after working for years or decades in their host country.

Chinese emigration to America: sketch on board the steam-ship Alaska, bound for San Francisco

A third wave of migration occurred for several decades after the fall of the Qing Dynasty in 1911 and was characterized by well educated professionals. Between 1920 and 1950, many of these immigrants were teachers who traveled to Southeast Asia to educate the Chinese children of families who had emigrated previously. A fourth wave of migration occurred after 1950 when Chinese in countries such as South Asia migrated to other foreign countries.

Since 1979, approximately 4.5 million Chinese students have traveled to the United States and other Western countries to seek university education. As China’s footprint in the world expands, educational destinations have expanded with it. Overall, according to UNESCO, in 2016 over 801,000 Chinese students pursued university education overseas. A significant minority of these students have elected to remain in their host countries at least for some period after graduation. For instance, the US Department of Energy’s Oak Ridge Institute for Science and Education noted that 92% of Chinese who earned science and technology doctorates in the United States in 2002 still resided in the US in 2007. Similarly, a 2013 National Science Foundation report noted that 86% Chinese science and engineering doctorate students hoped to remain in the United States after finishing their degrees. China has tried to reverse this educational brain drain by offering subsidies and perks for student returnees. Their efforts are beginning to show effects. The rate of return of overseas Chinese rose from a low of 25% in 2005 to 33% in 2010.

In 2000, the immigration rate of China’s highly educated population is now five times as high as the country’s overall rate. It is not just wealthy and middle-class students that are traveling abroad. Increasingly, middle-class and wealthy Chinese elites are increasingly pursuing work opportunities overseas or applying for immigrant investor visas where residency is offered to wealthy foreigners in exchange for a specified sum to be invested in the host country. In 2014, for instance, Chinese citizens received 85% of all U.S. immigrant investor visas. Wealthy Chinese cite several reasons for their wish to immigrate including the wish to join previously emigrated family members, pollution, poor food safety, weak rule of law and concerns about long-term political, economic and social conditions in China.

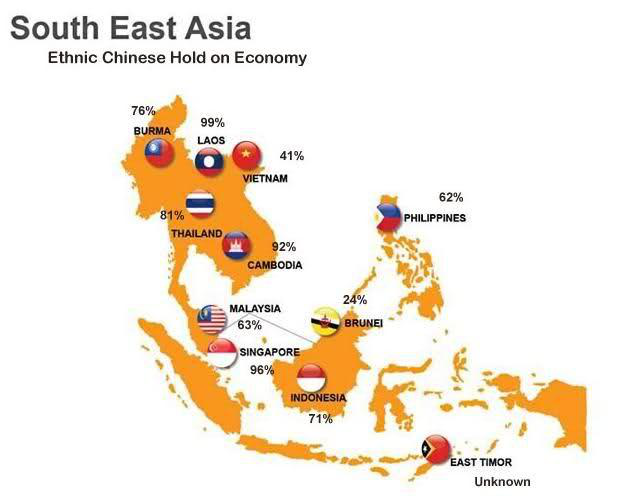

Chinese Diaspora and Economic Advantage in Southeast Asia

China’s emigration legacy has created immense economic advantage in many of the Southeast Asian countries. Except for Singapore, ethnic Chinese represent minority populations in Indonesia, Thailand, Malaysia, the Philippines, Myanmar, Vietnam, Laos, Cambodia and Brunei, but dominate the economic activity of their host countries. It is estimated that Chinese migrants control approximately 60% of the region’s private corporate wealth.

| Chinese in Southeast Asia |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ethnic |

|

|

|

|

Ethnic |

Ethnic |

Chinese % |

|

|

|

Host |

Chinese in |

Chinese % |

Control |

|

| Host Country |

|

Population 2011 |

Country 2011 |

Total (1) |

GDP Host (2) |

|

| Indonesia |

|

248,000,000 |

8,010,720 |

3% |

71% |

|

| Thailand |

|

64,260,000 |

7,512,600 |

12% |

81% |

|

| Malaysia |

|

28,730,000 |

6,540,800 |

23% |

63% |

|

| Singapore (3) |

|

5,260,000 |

2,808,300 |

76% |

96% |

|

| Philippines |

|

95,830,000 |

12,413,160 |

13% |

62% |

|

| Myanmar/Burma |

|

62,420,000 |

1,053,750 |

2% |

76% |

|

| Vietnam |

|

89,320,000 |

992,600 |

1% |

41% |

|

| Laos |

|

6,560,000 |

176,490 |

3% |

99% |

|

| Cambodia |

|

14,430,000 |

147,020 |

1% |

92% |

|

| Brunei |

|

410,000 |

51,000 |

12% |

24% |

|

|

|

|

|

|

|

|

| (1) Research by Poston and Wong: The Chinese Diaspora: The Current distribution of the overseas Chinese |

| (2) The economist later replicated by many sites |

|

|

|

|

| (3) % Ethnic Chinese calculated as % of Singaporean citizens not total Singapore population

|

|

Source: The economist

Activating the Chinese Diaspora

Since the fall of the Qing Dynasty in 1911, overseas Chinese have played an important in both the politics and economics of China. For instance, much of the funding for the 1911 Chinese revolution was donated by Chinese living abroad. After 1980, when China began undertaking economic reform, the People’s Republic of China actively recruited the assistance of its overseas population both in terms of skills and capital. More recently, China has worked to maintain the allegiance of recently emigrated Chinese, especially those professionals and students working and studying in foreign countries. Xi Jinping believes that the Chinese diaspora can play a significant role in helping China to reclaim its status as a premier nation both economically and politically. Overseas Chinese are some of the world’s most educated and successful professionals and entrepreneurs. With estimated total liquid assets of $1.5-2 trillion, the Chinese diaspora holds a substantial capital as well as expertise and relationships to be tapped for the continuing economic growth of the mainland. Additionally, it is estimated that the Chinese diaspora returns approximately $50 billion annually to China in terms of remittances.

In order to capture their expertise, Xi Jinping has launched a range of policies designed to encourage their continued engagement with the country. Such policies include the creation of over 200 Confucian institutes globally which have encouraged overseas Chinese to connect with their language, culture, homeland and each other. China has also been successful at encouraging ethnic Chinese to return to China to startup companies. Incentives proffered include the provision of free real estate or office space in high-tech parks, preferential tax treatment, preferential access to banking and credit, venture fund matching and streamlined regulatory processes. As an indicator of effectiveness of such policies, Greater Pacific Capital estimated that 25% of all tech startups in China are founded by returnees as opposed to home-grown entrepreneurs.

China has also worked to more effectively connect with the Chinese diaspora who intend to remain in their host countries. Programs include connecting overseas Chinese in academia and the science and technology sectors with their mainland Chinese counterparts as well as providing funding for their endeavors. Confucian Institutes help Chinese stay in touch with their language and culture while transmitting traditional Chinese culture and values around the world. Government web portals such as China Scholar Abroad and China Diaspora Web link ethnic Chinese with the mainland. The Chinese government has also hired top brand consultants and policy strategies to improve its international image and to advance policy agenda worldwide.

Additionally, China is also working at keeping it Chinese diaspora on message and sympathetic to China’s domestic and international policy objectives by creating a Chinese digital space where its points of view can be articulated. To this effect, China has acquired the control of newspapers, television stations and radio stations targeted toward the Chinese diaspora; it has used its economic clout to influence the reporting of independent media that have business ties with China; it has acquired both broadcast time and advertising space from existing independent media; and it has encourage ethnic Chinese to work in foreign media outlets in order to influence their reporting from within. Often, it has softened its messaging by placing its national goals under the banner of ethnic unity and common ethnic interests.

Trends

- A declining workforce will necessitate China to shift from a low-wage, labor-intensive model to a one where resources are used more efficiently, where there are increases in labor productivity, and where automation and robotics technologies help offset labor declines. There will also be pressure to increase the retirement age.

- The change from the One Child Policy to the Two Child Policy will result in only a small increase in China’s population.Significant socioeconomic changes that have occurred since the onset of the One-Child Policy have caused China to transform into a low fertility culture. These changes are consistent with the pattern countries follow as they become more developed.

- Going forward, China’s large population will continue to provide the country with enormous challenges. As its population continues to age, China will be challenged by slower GDP growth and the need to create pension and healthcare systems that will help relieve the burden of the young to care for the old. Additionally, China’s growing population, which is predicted to peak by 2035 at approximately 1.461 billion people, will continue to put enormous demands on its scarce natural resources. Water management, in particular, will be a huge future challenge.

- The challenges of China’s rapid urbanization are significant. Rapid economic growth will be necessary not only to the finance the enormous cost of this level of urbanization, but also to ensure that when centralized, urban populations do not protest government policy, as they did in Tiananmen Square in 1989. This could be a particular risk if long term migrant workers continue to be denied the same basic rights as registered urban residents, particularly as those urban residents will become an increasingly smaller percentage of the total urban population. Continuing to favor the original urbanites with government services risks long-term disadvantaging a large section of the population.

- Additionally, urban residents use, on average, 3.6 times as much energy as rural residents, creating greater demands on energy grids. Urbanization can also lead to greater motorization, taxing China’s new road infrastructure. Greater urbanization will also generate higher levels of pollution, further exacerbating China’s already polluted air.

- More changes in the household registration system, which identifies a person as a resident of a specific region—the so-called hukou reform—could accelerate the move of workers from rural areas to cities and help reduce the country’s growing inequality. HuKou reform will continue to proceed gradually, with second tier and smaller cities seeing reform while large metropolises such as Beijing and Shanghai keeping residence restrictions firmly in place. In the near term, urban hukouresidents will continue to get better ranking jobs, better wages, and benefits.

- China’s diaspora will continue to see growth in the coming decades. Part of this growth will be driven by university students continuing to remain in their host countries after graduation and part of the growth will be driven by wealthy and skilled professionals leaving China to seek better work opportunities and a better quality of life. Additionally, as China continues to build infrastructure globally, some Chinese migrants that have worked on the infrastructure projects will seek to remain in their host countries. For instance, it is estimated that approximately one million Chinese have emigrated to Africa since 2001. These immigrants have come both via state projects and via their own initiative.

- China will continue to activate its diaspora to achieve its domestic and foreign policy objectives. China views its diaspora as a source of capital and expertise. It also views it as a way to influence host countries from within.

References

")

China is answering these challenges by significantly investing in agricultural technologies including artificial intelligence, big data, robotics, and automation. Not only will these technologies help improve the efficiency and sustainability of China’s agricultural market, but they also represent a big and rapidly growing global business. The market for global agricultural robots, for instance, is projected to exceed $20 billion by the end of 2025, with growth in precision agriculture as a major driver. Artificial intelligence, automation, big data, and robotics are expected to find applications in everything from herding and fish farming to planting and harvesting. Other uses include seeding, irrigation, water leak detection, fertilizing, crop weeding, spraying, crop monitoring and analysis, disease and pest identification and eradication, thinning and pruning, and tracking the growth of plants. In addition to robotics, drones are also increasingly being used to monitor crops, conduct field analysis, manage livestock, plan interrogation and crop spraying. Drones aid farmers to see the big picture of their farmland and to make educated decisions that help to maximize crop yields.

China is answering these challenges by significantly investing in agricultural technologies including artificial intelligence, big data, robotics, and automation. Not only will these technologies help improve the efficiency and sustainability of China’s agricultural market, but they also represent a big and rapidly growing global business. The market for global agricultural robots, for instance, is projected to exceed $20 billion by the end of 2025, with growth in precision agriculture as a major driver. Artificial intelligence, automation, big data, and robotics are expected to find applications in everything from herding and fish farming to planting and harvesting. Other uses include seeding, irrigation, water leak detection, fertilizing, crop weeding, spraying, crop monitoring and analysis, disease and pest identification and eradication, thinning and pruning, and tracking the growth of plants. In addition to robotics, drones are also increasingly being used to monitor crops, conduct field analysis, manage livestock, plan interrogation and crop spraying. Drones aid farmers to see the big picture of their farmland and to make educated decisions that help to maximize crop yields.